AUS

Australia

AUS

Australia

IND

India

IND

India

UAE

UAE

UAE

UAE

CA

Canada

CA

Canada

SL

Srilanka

SL

Srilanka

Traveling abroad demands in-depth preparation in various aspects. The key among them are finance, housing, university or job, and of course, health. The last one seems to be more crucial in ongoing times like COVID-19 pandemic. Thus, your foremost aim should be to secure the best Overseas Health Insurance as per your current health condition.

Let’s start right from the basics. Why Overseas Health Insurance is necessary in Australia? Is it over – hyped? Is it compulsory and why? Can’t we just use Medicare? Is it necessary to extend health cover when we extend our visa?

Let’s take a while and know the answers to the most frequently asked questions when people relate the terms: Visa, Overseas Health Insurance, Australia, Compulsory, Cost & Comparison, Extending/Renewing OSHC/OVHC Insurance.

As many of us know, Australia is one of the few nations that brags about the level of medical facilities it provides to its people and citizens. The public health care system a.k.a Medicare, covers all doctor charges at public hospitals. It also reimburses as much as 100% of the Medicare Benefits Schedule (MBS) for a general practitioner and 85% of the MBS fee for a specialist. Medicare is not just about fee reimbursement or free treatment, it also encompasses eye tests, surgical procedures by dentists, various tests undertaken by patients such as X – rays, pathology tests etc.

However, Medicare stays limited to Australia and a few countries that has Reciprocal Healthcare Agreements (RHA) with Australia. Subject to various types of visa and policies, Australia has an RHA with countries like Belgium, Finland, Italy, Malta, Netherlands, New Zealand, Norway, Ireland, Slovenia, Sweden and United Kingdom.

The healthcare system in Australia is dear and can account for massive out-of-pocket expenses if not covered with appropriate overseas health insurance. One day at a hospital in Australia with a private bed and consultations could cost a person as much as $1000

Must Read: With OSHC, Secure Your Health and College Life In Australia

As various types of visas have various health requirements, it becomes important for us to check the requirements as stated by the Department of Home Affairs, Australia. Let’s understand some of them.

- All student visas, under subclass 500, requires students to have and maintain an OSHC Health Cover during their entire period of stay in Australia. The ONLY exemptions for an OSHC insurance is if students are from Norway, Sweden or Belgium – covered under various agreements. To everyone else, it stands compulsory.

- Students under Temporary Graduate Visas, under subclass 485, are also mandated to have an adequate OVHC insurance (Overseas Visitors Health Cover) during their stay in Australia. If the applicant hails from the country Australia has a Reciprocal Healthcare Agreement (RHA) with, they might be covered under Medicare.

- For Visitor visas, under subclass 600, are not mandated to possess an Overseas Visitor Health Cover (OVHC) insurance however, it is recommended not to travel without one unless you wish to spend $1000-$2000 everyday unnecessary.

But insurance once done is done. No need to extend or renew, right? Well, you may want to re-think and do things differently.

Sam is studying in Australia and rightfully has an OSHC insurance to save him from medical expenses. He wishes to extend his stay and pursue Masters to have better career prospects.

His friend Bert, who is working in the university library is going through the same conundrum to extend his working visa.

So, what do they do? Can they extend their visa applications without extending their health insurances? The answer is simple. No, they can’t.

When one renews their student visa or working visa, they also have to renew their OSHC or working visa health cover. They have to have the relevant overseas health insurances till the date they wish to stay in Australia.To make the matter simple, Sam can visit GetMyPolicy.online to view, compare & buy the best health policy as per his needs to renew OSHC insurance. Similarly, Bert can renew his working visa health cover and align it with his needs and specifications by comparing various plans from visitors’ insurance providers. GetMypolicy.online enlists all the government-approved OSHC like Ahm, Allianz Care, Bupa OSHC, Medibank, Nib etc.

With the renewed status of their respective overseas health insurance, they will be eligible to extent their visa. But hey, what happens if they forget to renew their health covers?

In Sam’s case, if his student health cover expires when in Australia on a student visa, he can still renew OSHC insurance for the rest of his student visa, but will have to pay the premiums for the gap period when he did not have the cover. He will also not be able to claim any benefits during the expired period of his student’s health cover.

In a similar fashion, if Bert’s OVHC insurance policy expires when he’s in Australia on a working visa, he will still be able to renew OVHC insurance. However, if his visa expires, it will be termed as invalid and he will now have to appear for a new visa. It would have been ideal for him had he renewed the same before the expiry of his existing working visa. Moreover, he’ll need to keep in mind to not only to extend his working visa in time but also renew OVHC insurance before it gets lapse.

Must Read: Most Important Terms to Consider for Australia Health Insurance Plan

This post is all about how international students can claim their pharmacy expenses based on their OSHC Insurance.

Before we begin, one ought to understand what is PBS?

PBS stands for “Pharmaceutical Benefits Scheme” is an Australian Government program that benefits Australians as well as visitors by subsidizing medicines to make them more affordable.

The PBS is governed by the National Health Act 1953. Details about the Minister for Health are available on the Department of Health website.

OSHC for Australia is mandatory for students to keep for the entire length of their student visa. In short, OSHC insurance is a visa-length cover. Pharmacy bills containing prescription medicines prescribed by a doctor/GP while in Australia are covered under your OSHC Health Insurance.

PBS prescriptions are always accompanied by co-payment. For now, major OSHC providers have set the minimum co-payment amount for the international students to $42.30.

If the cost of a PBS medicine falls below the general co-payment amount (under co-payment prescription), the method used to calculate the maximum general patient charge for the medicine includes an Additional Fee, an Additional Patient Charge, and any applicable price premiums.

To claim the pharmacy expenses, a student first has to pay the co-payment of $42.30 (counted towards each item in the bill) & the rest will be paid by the OSHC provider up to a maximum limit of $50 per prescribed item.

Later, the student has to contact OSHC health insurance provider to start the claim process for reimbursement. We hope that the pharmacy expenses claim process for OSHC policy will be easier to understand with the following infographic.

Do you always feel “tumbling down the rabbit hole” because of the complex terms involved whenever you need a new or extend your health insurance plan?

Well, relax. We have got you covered in this post.

Australia requires you to have OSHC (overseas student health cover) for students and OVHC (overseas visitor health cover) for working and visitor visa categories.

Choosing the right overseas health insurance can be an intimidating process for aspiring & existing international students because it demands to figure out which policy is the best one.

Aspiring migrants who want to settle down in Australia also face the same issue with buying adequate health insurance (OVHC) to meet the Australian visa requirements.

Australia boasts one of the best health & medical facility across the world and thus; one must require to have the specific level of health insurance (OSHC and OVHC) for themselves as well as the family members for the entire duration of stay in Australia.

Among many others, the leading government-approved health providers are Ahm OSHC, Allianz Care OSHC, Bupa OSHC, Medibank OSHC, and Nib OSHC. ensures the best coverage against hefty medical and hospital accommodation bills that usually occurs due to some situations that we compiled in another blog.

Buying health insurance is a tricky deal to crack, to be honest. No one wants to regret their decision after investing the money. So, it is always recommended not to get overwhelmed with the information available in the market and ever think about the actual need before buying a policy.

This is attributed to a number of questions asked related to health or the use of medical terms that certainly gives a hard time to understand and make the buying process insanely confusing.

Besides, people often confuse “benefits” with “returns”. Even though health insurance is considered an investment, it is strictly limited to risk protection and not increasing your savings.

Are you also looking to buy the best overseas health cover and want to avoid the same consequences? You need not panic.

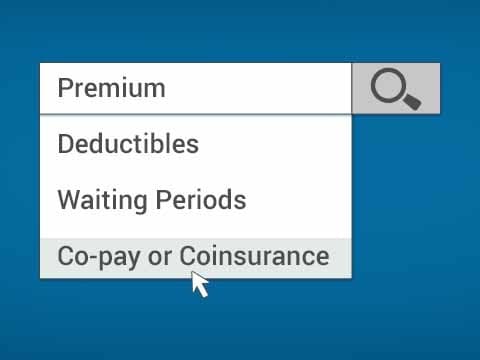

Let’s start with the 7 points that one must consider before buying an overseas health cover. Take a look!

1. Coverage: Are you among the ones who prefer to buy a overseas health insurance just because it’s less expensive? If yes, then you may have to rethink. One must not purchase a plan just because it is less costly but carefully measure the amount of coverage it offers.

Some of the incentives to ask the insurance provider are pre-hospitalization and post-hospitalization, network hospitals, day-care services, free medical check-ups, maternity benefits, amount of money for claims, etc.

2. Premium: Before buying overseas health insurance, one must calculate the premium. Premium is the amount you are required to pay for your health insurance coverage, typically every month.

You need to decide how much you can afford to spend on your policy since each insurer has a different set of standards and assumptions to measure the premium amount, and if you fail to pay that amount you risk losing coverage.

3. Deductibles: A deductible is a specific amount that a policyholder pays each year towards the medical expenses before the insurance provider proceed to provide you with the benefits.

For example, you buy an annual $1000 deductible health cover and a hospital stay that will cost you $20,000. Yeah, you’d only be responsible for paying $1000, and the health plan will start paying the premiums for the remaining $19,000 as per the contract terms and conditions.

The primary purpose of having a deductible is to keep the premiums low through cost-sharing and reduce the number of small claims.

4. Waiting Periods: While purchasing an overseas health cover, one has to keep in mind the waiting period. All health cover plans come with a waiting period for pre-existing diseases like diabetes, high blood pressure, thyroid, etc. It is a specific period that you need to cover before claiming any benefits in your insurance policy.

Generally, a waiting period of 2 to 4 years is a standard clause in the majority of the health policies. When you abide by this clause (i.e. serve your waiting period), you will never be denied for appropriate claims by the insurance companies.

Must Read: Know more about Waiting Period

5. Co-pay or Coinsurance: Co-payments are the fixed amount of cost-sharing between the insurance provider and the policyholder for specific health benefits or drugs. For example, you purchase a policy for primary care doctors with $20 co-pay, and generic drugs with $10 co-pay. For those facilities, you have to pay specific fixed amounts regardless of the cost.

More often, people confuse co-pay with deductibles, but, they are entirely different terms. A co-pay is the fixed amount that you pay each time you get a particular type of health service. While a deductible is an amount that you pay annually before actually reaping the benefits of your health insurance cover.

6. Sum Insured: Sum Insured is the guaranteed amount of money an insurance company assures to pay when a claim is made. When choosing a ‘Sum Insured’, you need to consider your age, income levels and add-on covers in the policy as it also affects your premium amount. It is always advisable to take care of medical inflation in order to make the most of the sum insured.

7. Exclusions: Before purchasing the policy one must check the exclusions. Exclusions are the disease, situation or condition that is not covered by the insurance provider and those medical costs are totally upon the person. Exclusions can be either ‘permanent’ or ‘first year’. Permanent exclusions are never covered whereas the first year exclusions will be hidden from the second year.

Now that you are aware of these terms and before you leave us to buy one, why not compare multiple plans first at www.getmypolicy.online and be sure of making a right decision!

On GetMyPolicy.online, you can compare the plans from leading service providers in Australia and get the best quote, be it for 485 Visa, 489 Visa or student visa. Through this platform, you can purchase the overseas health insurance from Bupa (OVHC & OSHC), Allianz Care (OVHC & OSHC), Ahm (OSHC), Medibank (OSHC & OVHC) and Nib (OSHC).

There are no hidden overheads, just the platform with the most accurate information and hassle-free buying process.

Start navigating now to get the best value at the least price!

When it comes to buying overseas health insurance there are a lot of decisions to make. One of the most important is whether you should buy individual or couple’s coverage.

This article will discuss some of the major differences between these two types of policies so that you can make an informed decision about what type of overseas health insurance is best for your needs.

What is Couple Overseas Health Insurance?

The idea of private health insurance is to offer you and your partner protection against the costs associated with hospitalization, doctors’ appointments, out-of-hospital medical services like dental care or physiotherapy that aren’t covered by Medicare.

Outsmarting these expenses can be difficult for many people who are on tight budgets. Thus, it’s important not only to have this type of coverage but also to investigate what else might apply to get full value from insurers including the extra cover which offers help paying bills when emergencies arise.

How Does a Couple OSHC Policy Work?

If you’re legally married or in a de facto relationship, then there are two options for couples’ health insurance. One is to take out separate policies and buy them together as partners; the other would be getting one policy that covers both of your needs under this arrangement.

What is Single Overseas Health Insurance?

A single health insurance policy will cover one person instead of multiple people. This means it can be more tailored to the needs and preferences of that specific policyholder, as opposed to needing what benefits parents or spouses may need to maintain their families’ coverage.

What are Hospital Cover & Extras Cover?

Hospital Cover

Hospital insurance is a great way to protect yourself from high medical costs. Hospital policies can cover the cost of treatment when you are admitted as either an in-patient or outpatient, including doctor visits and hospital stays!

- theatre and hospital accommodation fees

- patient meals

- intensive care

- prostheses objects

- diagnostic tests

- drugs, dressings, and other medical supplies

Extras cover

A person with OSHC for Australia with Extras cover will be able to pay for out-of-hospital medical services, such as:

- dental treatment (including dental check-ups)

- optical including eye check-ups, glasses, and contact lenses

- orthodontic treatment

- chiropractic treatment

For people who question the need for an OSHC cover, a private bed at an Australian hospital with basic medical facilities could cost you as much as 1000 Australian Dollars a day. Too much of a ‘hole in the pocket,’ isn’t it?Answering your question with basic statistics, if an overseas student looks to buy an OSHC, say, for one month, it costs, at an average, approximately AUD 41. (Varies as per the OSHC provider) Therefore, for a two–year course, a person would end up paying close to 1000 AUD. Again, two persons would end up paying 2000 AUD for the same.

However, in case a couples’ OSHC insurance is taken, for the same month taken for individual calculation, it would, at an average end up costing them AUD 250 for a month and as much as 3000 AUD for a year. And, for the similar case as mentioned above, a whopping 6000 AUD for a 2-year course!

Just have a look at what has been highlighted. Do you realize that the insurance covered is the same, for the same number of people – two? Then how come the couples’ insurance is three times the cost of 2 individual student insurances? Conventional thinking, however: Isn’t it economically feasible to buy two such individual OSHC policies? Smart savings, right?

Well, there is a clash of thoughts! As per the Australian home affairs, the OSHC policy for families or couples need not be combined, and each applicant can take out their covers respectively. (Economically simple and feasible, isn’t it?) But keep in mind, that in almost all cases, the department of home affairs doesn’t have anything else to do wrt. Individual/couple insurance as their primary concern is addressed – You have made arrangements for adequate health insurance for your period of stay in Australia.

However, the policies of insurance companies seem to collide with this view of thought. As per them, a couple is not allowed to have dual individual policies. They MUST have the couple’s insurance.

There is NO CLEAR REASON for the extreme difference in prices, however. Here are a few possible reasons:

- You might take up two individual policies, but the insurance provider could annul the benefits of the claim on the pretext of a wrong insurance cover.

- The reason for the price difference could be covering pregnancy & infant – treatment costs by the insurance provider. This again collides with a couple who don’t intend to have a baby during their months of study in Australia. In such cases, there would be unwanted high payments.

Must Read: Pregnancy Care in OSHC! Essential Things You Need to Know!

- Even though individual policies are liable to get their visa approved, problems could arise in case of bill clearances. Also, if one of the two members or both visits a doctor, they could still be denied coverage on the pretext of possessing incorrect insurance.

- In the case of individual policies, your dependents are not covered if there is a need for prolonged treatment. This could result in excessive costs being made out of pocket and worse, you wouldn’t even be able to claim for it.

Wrap Up:

Whatever your choice is, we are here to help you. At GetMyPolicy, choose between the best government-registered insurance providers and plans. Also, compare between them, see available features, and know precisely what you pay for. That is not all. Upload your policy and get 15 FREE PTE Practice Tests!

Uday’s (name changed for privacy) parents visited Australia first time in 2014 on tourist visa. They got an insurance policy from a reputed Indian insurance company before arriving in Australia.

When they arrived in Australia, they found the claim process of current health insurance to be lengthy and tedious hence they were unsure to continue further with the company.

Their son Uday did a research and found out an Australian company’s policy that covered most of the things like ambulance services, general dental, optical, GP visits etc. Hence, he got a bronze visitor + extras couple cover at the monthly premium of $356. Uday’s father also informed about his condition of prolonged diabetes as it is one of the mandatory requirement before getting a health insurance policy.

While Uday’s father was in Australia, he suffered from a sudden heart attack and needed emergency medical treatment. The total hospital expense for the entire treatment was $32,000. After the payments were done, the family went to the Australian insurance company for the claim. While processing the claim, the company studied the medical reports.

During the initial investigation, The insurance provider surmised that since Uday’s father was suffering from prolonged diabetes, his heart ailment might be a pre-existing condition which was not declared while getting the policy. Further to their investigation, they asked Uday to submit previous medical records to which he agreed and followed all the procedures without any deviation.

Uday submitted all the previous medical records of his father. After a quick deliberation, the insurance provider came to the conclusion that the pre-existing condition clause doesn’t imply here and hence Uday and his family were eligible for the cover of $18,000 under the restricted clause for cardiac arrest treatment (in accordance with the claims standard set forth for the bronze cover). This was a great help for Uday and his family as the insurance company paid a huge sum of the medical expenses as promised.

Since, Uday made the right decision of moving to an Australian insurance company, it helped him to deal with the large sum of emergency medical expenses. Now his parents keep visiting Australia after every 6 months.

When his parents are not in Australia, he blocks the membership which means he doesn’t have to pay the monthly premium of $356 for that duration. When they are back in Australia, he unblocks the membership and his parents are again covered by the policy. Hence this Australian company’s policy was ideal for him and his family.

If you are also living in Australia and have parents who need to visit you frequently, with a right level of health cover you can make sure you and your loved ones are covered in case any injury or accident happen.

Being a group of professional immigration consultants, we at Aussizz Group always work by the sweat of our brow to make sure our client fulfils every obligation to migrate to Australia and have a peaceful stay here. Apart from providing assistance for the visa process, we also extend our support in choosing the best health cover for them and their dependents.

At GetMyPolicy.online you can find a great range of health insurance plans by leading providers of Australia. You can compare them at different parameters like premium, deductibles and choose the one that best meet your needs.

South Australia has unveiled its Skilled Occupation List for 2023-24 (General Skilled Migration program), introducing a Registration of Interest (ROI) system to manage the influx of potential applicants. This system is designed to balance the high demand from individuals residing and working in the state with the limited availability of nomination slots.

Registration of Interest (ROI) Process:

The South Australian Government has transitioned to an ROI process to streamline applications. This implies that aspirants are required to submit an ROI and await an invitation to apply for state nomination from South Australia, prohibiting direct applications for state nomination.

Priority to International Graduates and Temporary Visa Holders:

South Australia is emphasizing the retention of its international graduates and temporary visa holders, prioritizing them under this invitation process. This approach ensures that the state retains a diverse and skilled workforce, contributing to its overall development and growth.

Targeting Experienced Overseas Workers:

The state is actively seeking experienced overseas professionals possessing skills in sectors experiencing high demand in South Australia. Professions within Trades and Construction, Defence, Health, Education, Natural and Physical Science, and Social and Welfare are particularly targeted. These individuals are approached through invitations to apply for South Australian nomination, ensuring the state has access to a pool of skilled and experienced individuals.

| Nos. | Occupation Categories | Nos. | Occupation Categories |

| 1 | Farmers and Farm Managers | 13 | Construction Trades Workers |

| 2 | Specialist Managers | 14 | Electrotechnology & Telecommunications Trades Workers |

| 3 | Hospitality, Retail & Service Managers | 15 | Food Trades Workers |

| 4 | Arts & Media Professionals | 16 | Skilled Animal & Horticultural Workers |

| 5 | Business, Human Resource & Marketing Professionals | 17 | Other Technicians & Trades Workers |

| 6 | Design, Engineering, Science & Transport Professionals | 18 | Health & Welfare Support Workers |

| 7 | Education Professionals | 19 | Protective Services Workers |

| 8 | Health Professionals | 20 | Sports & Personal Service Workers |

| 9 | ICT Professionals | 21 | Office Managers & Program Administrators |

| 10 | Legal, Social & Welfare Professionals | 22 | Other Clerical and Administrative Workers |

| 11 | Engineering, ICT & Science Technicians | 23 | Sales Representatives & Agents (Insurance, Real Estate) |

| 12 | Automotive & Engineering Trades Workers |

For more information on the Skilled Occupation List: https://www.migration.sa.gov.au/occupation-lists/south-australia-skilled-occupation-list

Contribution to Fast-Growing Industries:

South Australia is on the lookout for highly skilled overseas workers capable of significantly contributing to the state’s rapidly expanding industries and nationally prioritized projects. The focus is on individuals with experience in the defense industry and those with specialized skills in digital and critical technologies sectors. The inclusion of such skilled individuals is crucial for the state’s progression in these pivotal sectors.

Opportunities for International Graduates and Temporary Visa Holders:

International graduates and other temporary visa holders are evaluated across a wide range of occupations, maintaining consistency with previous years. Moreover, over 290 occupations are available to offshore skilled workers, offering a plethora of opportunities for individuals around the globe.

2023–24 Business Innovation and Investment Program:

Currently, South Australia is not accepting applications for state nomination for the Business Innovation and Investment (Provisional) visa (subclass 188). However, business or investor migrants possessing a provisional visa (subclass 188) are eligible to apply for nomination for the extension stream or permanent visa (subclass 888) in 2023–24, as these are not constrained by a nomination cap.

South Australia’s Skilled Occupation List for 2023-24 and the introduction of the ROI process mark a strategic approach to managing the demand for state nominations. By prioritizing international graduates, temporary visa holders, and experienced overseas workers, South Australia is fostering a diverse and skilled workforce to drive the state’s growth in various high-demand sectors. The opportunities presented by the state are extensive, spanning across numerous occupations and industries, and are set to play a pivotal role in shaping the state’s future landscape.

Application Fees:

For more detailed information regarding application fees and any other associated charges, please do not hesitate to get in touch with us. We are here to assist you with any queries or clarifications you might need.

Content Courtesy: https://www.migration.sa.gov.au/news-events/2023-24-general-skilled-migration-program-now-open

Ahh! That’s just the visa requirement! I’ll buy the cheap health insurance policy.

Most often, people looking to study or work in Australia have the same thought when they are asked to have an OSHC (Overseas Student Health Cover) or OVHC (Overseas Visitor Health Cover) to meet the health requirements for visa.

There is a tendency to look for options which are relatively cheap or suitable to the pocket or buying the one without knowing the details of varied health plans available as per the personal requirements. As a result, they don’t get the right kind of financial assistance when any mishap or unfortunate situation happen.

However, it is of utmost important to take a number of aspects into consideration before buying or even renewing your health insurance policy. It is only then, that you can zero in on the right policy for yourself as well as your family.

Let us look at some of the most common mistakes people make, so that you can avoid them when you decide to choose the ideal health plan for yourself to apply for any Australian visa.

1) Caring for Money over Coverage

Whenever you buy anything, you must look at the money aspect of it; that is only natural. But, unlike any other things and services available in the market, which you can choose primarily based on their cost, you cannot do the same when you’re out there choosing a health insurance plan.

The reason is simple. The right plan might not seem too important in your normal routine life, but it is meant to protect you from falling into undue financial circumstances at the time of a medical emergency.

The word ‘emergency’ is important here. So, do not choose a plan with an insufficient coverage, to save yourself a financial inconvenience now; because it could cause a bigger mess when you’re already inconvenienced health-wise.

2) Always looking for the basic cover

A health insurance plan has to be comprehensive in its nature; otherwise, what’s the use? Most people, when they decide to buy a plan, are so adamant on saving a few bucks, that they tend to choose a very basic plan over a detailed one.

If you’re buying an insurance plan, just for the sake of it – it is almost as good as not having one. If you fail to realize how big a role a comprehensive insurance plan can play towards helping you out in your need of hour, then it is a matter of concern.

The right way of going about this is through choosing a plan that covers a critical illness rider and a personal accident rider, in addition to the basic insurance plan. A complete plan is one, which also provides you with certain added benefits, such as cashless hospitalization, domiciliary hospitalization, and ambulance charges.

3) Not Reading Every Claim Properly

To err is human, they say; and when it comes to making an error while reading the fine print on your insurance plan, misunderstanding something, or leaving something out completely – is an error not too uncommon. Just so that you don’t have to face any problems due to that, later on, you’ll find almost every health insurance company providing a 15-day ‘look period’.

As the name itself suggests, this is a 15-day time you get, after you have already bought your policy, to look at the fine print, and understand each detail properly. This is a free look period, at the end of which, if you do find something problematic, you can ask for your plan to be scrapped right then.

The company will initiate the cancellation procedure, and offer you a payback as per their Terms and Conditions. This period is extremely important ; and do not waste it. Make sure you have gone through each and every clause, before you agree to go further with the plan.

4) Hesitating in Going for a different Insurer

For some reason, people feel a bit shy when it comes to changing their insurance provider. The question is, why? If there is another provider who’s offering you a plan with better benefits, you should not refrain yourself or hesitate from reconsidering your current plan, and skip to the better one.

5) Keeping Certain Things from Your Insurer

Do not conceal any medical facts about yourself. If you keep any of your health conditions undeclared in front of your insurance provider, at the time of purchasing a plan, you might face problems ahead. This could be held against you, at the time of claim settlement.

For instance, if you are suffering from a pro-longed illness but you didn’t bother to mention the same in your application. And by any chance if you are hospitalised due to medical emergency, your claims get rejected on sending the hospital bill to the insurer.

6) Delay in Renewing the policy

Without the proof of adequate health, overseas visitors and students cannot spend a single day in Australia. If you fail to renew this policy means you are breaching the health insurance condition, which ultimately result into visa rejection or cancellation. That’s not all, there are also other disadvantages if you renew the policy after the due date. To know them visit now

Must Read: Why Renewing OSHC & OVHC Is Significant to Ensure a Continuous & Stress-Free Stay in Australia?

Whether you are traveling for weeks, undertaking a course of study for few months or living for years, considering an international health insurance carefully is essential to prepare for or avoid potential dangers. Discussed above are a few things that people take for granted, while choosing an OVHC policy or OSHC policy. We hope you don’t make the same mistakes and buy the one that covers the maximum benefits you need.

If you want to compare health insurance plans before making any decision, then www.getmypolicy.online is the perfect resource for you . It allows you to compare a wide range of health insurance plans by Australia’s leading providers like Allianz Global Assistance, Bupa, Nib and AHM and buy the one that perfectly meet your needs along with the immigration department for Australian visa.

You started your international journey in Australia with a great fervour.

You worked tirelessly to make the most of every opportunity coming your way to build a successful career in Australia.

This began with choosing a course that can help landing a dream job in future, dealing with months of preparation for visa and getting acquainted with the international practices.

But, what if the immigration department ask that you cannot live or extend your stay in Australia?

You are sitting, contemplating with shock – despite having a valid visa, best financial support, required skills, Why I am not eligible to stay in the country?

Well, It’s because of the Expired Health Insurance Policy!

Being a migrant in Australia, you will obviously be aware of the importance of having an OSHC (Overseas Student Health Cover) and OVHC (Overseas Visitor Health Cover). It is one of the mandatory requirements for a work or student visa of Australia to fulfil, as it provides access to high quality health care and coverage against unexpected medical expenses. Failing to maintain an adequate level of health cover, means not meeting the health requirements for Australian visa, which ultimately results into visa rejection.

When it comes to purchasing OSHC or OVHC, we leave no stone unturned to buy the one that best meet our needs and budget. We make sure to consider what the plan covers, compare benefits and figure out the premiums meticulously.

However, we completely overlook some factors that make us deprive of enjoying the continuous benefits of our health insurance plan. One of them is renewing the policy before the due date or expiry date.

Why Renewing Your OSHC and OVHC Is Important?

All the health insurance policies come with an annual limit and hence need to be renewed every year. If you fail to renew the policy before the due date, the negligence may cause a policy lapse and need to buy a new one.

It also goes with Overseas Student Health Cover and Overseas Visitor Health Cover. Insurance companies in Australia work closely with the Department of Home Affairs to monitor the compliance of health insurance. If you are on Australian student visa or work visa, you cannot spend a single day without having an evidence of suitable health cover arrangements. So, be sure of not missing the due date to ensure a continuous stay in Australia.

Even though the insurers send a renewal notice informing the insured about the expiry of the policy, it is the responsibility of the insured to renew the policy within the stipulated time.

Other Consequences

- No-Premium Benefits: When you purchase a health insurance policy, a premium is paid to the insurer every month to avail coverage benefits during critical times . In case, the policy terminates due to non-renewal of policy, you also lose the premium benefits. And even you renew the policy after the due date, you need to pay the interests as well, which obviously proves to be more expensive.

- More Waiting Period: It is evident that the insured need to serve a designated waiting period to avail certain benefits under the health insurance plan. If the policy lapse, you will have to serve that waiting period all over again to claim that benefits and face many other problems in an international country when an emergency situation arises.

- Pre-Existing illness cover: As we read above, with a new policy also comes a new waiting period. This is also applicable to the pre-existing illness cover. One has to wait for two to four years to avail that coverage. So, even if you have served this period with your old policy but failed to renew the policy on time, the same period will be count with a new policy to make you eligible for the coverage of pre-existing illness.

Must Read: What is waiting period in OVHC and OSHC?

Things to Consider When Renewing a Health Insurance Policy

- Grace Period: Generally, if the insured fail to renew the policy or pay premium by the deadline, he is given a grace period of 15 or 30 days by the insurance company. If you renew your policy within that time-period, your policy will be considered valid and make you eligible to enjoy benefits.

- Reconsider Your Health Insurance Requirements Carefully: Being a policy holder, you must inform about any change in the health condition to the insurer. It is the time where you need to choose the coverage that can help to meet your family’s financial needs in Australia. It can either be adding a new child/spouse or removing an expired member from the coverage.

- Insurance Provider: Many times, in health insurance case, we often feel to switch to better options or services than the one we currently possess. If you too feel the same, you can switch to other policy or change your provider. You can also refer GetMyPolicy.online to compare multiple plans by leading health insurance providers and choose the one that can best protect your journey in the ‘land down under’

** If your request to switching to other policy or provider is not in line with the company’s terms and conditions, it may get rejected. Some other common reasons responsible for the rejection are insufficient information, poor claim history, missing previous policy document, higher age, etc.

Getting a chance to study and settle in a country like Australia is an opportunity that doesn’t come frequently. You are ought to fulfil all the obligations and laws so that it does not hamper your goals or career. Having the health insurance renewed on time is such obligation to follow as it saves you from facing horrible consequences and allow you to stay stress-free in an unknown country.

When it comes to visiting overseas temporarily, people have a tendency to buy health insurance cover without knowing the importance of getting familiar with the level of coverage.

This is the reason that despite of getting an adequate level of health coverage from home country, they don’t get covered for the medical expenses overseas or get the very minimal level of coverage.

One of our clients, Mr Priyank (name changed), is a testament to this fact. He had a difficult experience with an Indian insurance company.

Mr. Priyank visited Australia to see his son on a visitor visa. He took an insurance out for both him and his wife with an insurance company in India. During his travel, he contracted Malaria and had to be hospitalised as soon as he arrived in Australia. He had to bear the initial expenses by himself by paying from his pocket, as Indian insurance companies cannot participate in bulk billing arrangements and money can be recovered by filing claims later.

The expenses came out to INR 1,20,000 which included expenses for medical admission in to hospital, pathology tests and treatment for malaria.

Thanks to his son who is a resident in Australia, Mr. Priyank was able to manage these unexpected expenses in Australia. Mr. Priyank gathered all the paperwork meticulously to make sure that he could file his claims with the insurance company once returning to India.

But the litigation process with the insurance company took nearly 10 months to recover most of his money. Mr. Priyank was able to get INR 1,12,000 of his money back but in bits and pieces and only after aggressive follow ups from his end. He could get an initial Rs 28,000 through a quick reimbursement process after which the file was put on hold for extended periods.

Standard documents were repeatedly asked making the paperwork lengthy. The rest of the money came in parts, sometimes forgotten by claim officers and a partial amount will only be transferred after the insurer tracks his impending payments. The process was stacked up against the insurer to basically make them give up on claims by making them undergo a long and contrived process.

However, getting an Australian visitor cover means access to bulk billing medical outfits, emergency services, hospitalisation etc. Also the claims process is fairly simple and done in a steadfast manner.

At Getmypolicy.online, you have the privilege to compare a wide range of plans by leading insurance providers of Australia and choose the one that best protects your stay and visa requirements. There are no hidden costs, you can purchase the desired health cover in minutes due to unbiased information and simplified buying process.

Getting a health insurance to visit or live in Australia is a thing that is often overlooked or given a less importance.

Even though it is one of the mandatory requirements to fulfil, a certain misconceptions revolve around the aspiring immigrants when it comes to buying an Overseas Visitors Health Cover.

This includes:

“Cheap policy will work for me as I am young and healthy”

“I have enough funds to face any emergency situation. I don’t need to go for higher coverage”

If you are also contemplating around such thoughts, then you ought to read this story.

This is a true story of Arjun (name changed for confidentiality) from India, who like any other professional, was excited of getting an opportunity to work in Australia on 457 visa.

He migrated to Australia with his family in 2012 and was really overwhelmed with his achievement. He had everything on the table from the academic documents, employer sponsorship and health insurance (OVHC).

Little did he know, his preferences in choosing the health cover, would lead him face horrible consequences.

But where did his choices go wrong?

Without understanding the implications of choosing the wrong OVHC plan, Arjun chose to go with the cheapest policy all because he wanted to save some money.

After Arjun arrived in Australia, within one year, he was detected with a life-threatening disease “Blood Cancer”. This was a devastating situation for the entire family.

His only ray of hope was that he and his family were covered for the medical expenses in Australia.

But, Arjun’s health insurance policy only covered the basic services and not the expenses for the treatment of bone marrow transplantation. He needed chemotherapy and radiation along with the support of highly trained medical professionals for a huge operation.

The Health care was definitely very expensive and hard to afford for Arjun and his family. He updated his plan to a platinum visitor cover as this will cover all the treatments including bone marrow transplantation in Australia.

Unfortunately, updating a cover didn’t come for a rescue too for the family as the policies don’t cover existing illness for at least one year. There is a waiting period of 12 months to get the privileges of that cover.

Due to all these circumstances, he couldn’t afford to get treated in Australia, hence he had to fly back to his country for emergency treatment. He was only able to return to Australia after one year.

His wife who was working as Chef lost her job. Their children had to repeat a class. They had to start from scratch in an international country.

Fighting with a fatal disease with no support led the entire family with a severe psychological breakdown. Thankfully, Arjun’s family pulled through this crisis and Arjun emerged as a true fighter and survivor!!!

What happened in Arjun case, will not happen in everyone’s case. But do we have to wait for that situation to occur? Of Course Not!

So, make sure you choose the health insurance for your Australian visa that protects you the best and your family.

At GetMyPolicy.online, you can compare a wide range of OVHC & OSHC policies on different parameters like coverage, waiting period, emergency services, accommodation, etc and get the best quote at just one click.

Visit now and mitigate the risk of paying hefty medical costs for your entire duration of stay in Australia.