AUS

Australia

AUS

Australia

IND

India

IND

India

UAE

UAE

UAE

UAE

CA

Canada

CA

Canada

SL

Srilanka

SL

Srilanka

The thought of studying and getting a degree in Australia triggers endless number of questions in the mind of an international student.

Some of the common ones are:

How will I find accommodation?

What if I face financial problems there?

Will I be able to overcome the language barrier?

How will I make arrangements for the sufficient level of Health Cover?

This is also followed by edginess of going through months of paperwork and applications, travelling thousands of miles and undertaking the challenging course of study.

While getting solutions for these concerns certainly pave the way to ensure a smooth transition to the “land down under”. There’s one question that rarely comes up but has a huge impact on your international journey.

What happens if you become pregnant while studying in Australia?

No doubt the situation is relatively rare, it does happen, whether it’s planned or unplanned. And falling pregnant while you study in Australia greatly affects your student visa.

Let’s see how!

It is evident that international students must have adequate level of Overseas Student Health Cover (OSHC) to meet the medical and hospital care costs in Australia.

Must Read: Why Overseas Student Health Cover Is Necessary to Get Australian Student Visa

This health cover clearly specifies that pregnancy is not covered for international students with the exception of emergency medical situations that may arise.

Not having a sufficient level of health cover for the duration of stay in Australia means breaching the condition 8501, which ultimately results into the cancellation of visa.

Hence, it is essential to know OSHC policies thoroughly including the pregnancy related services along with the childbirth.

Upgrading the OSHC Policy

OSHC comprises of three policies- Single, Dual and Multi-family. If you fall pregnant in Australia, you need to upgrade your policy before the baby is born.

If your policy covers the benefits for a single person, you need to upgrade to dual or multi-family policy.

If you are on dual family policy and have one spouse or recognised de-facto and more than one dependent child in your policy, you need to upgrade it to multi-family policy. Both dual and multi-family policy will increase the amount of premium you pay for the policy.

However, if you are already on multi-family policy, you just need to add baby in your policy and there will not be any changes in your premium.

The policy must be upgraded within 60 days of baby’s birth date to avoid waiting periods and ensure baby is covered for medical services that may need.

Once the baby is born, all you need to do is to contact your OSHC provider to add him/her in the policy.

Choosing the Hospital

One can choose to have baby either as:

- Patient in public hospital OR

- Patient in private hospital (Gap fees & out-of-pocket costs applicable)

Types of Pregnancy Care Covered in OSHC Policy

In Australia, pregnancy care is provided by obstetricians, doctors or midwives.

You need to consult your local doctor first and get recommended for the services of an obstetrician or qualified midwife. Such individuals partake in a shared maternity care program to manage pregnancy. That practitioner or specialist you choose will then be responsible to see you on a daily basis throughout your pregnancy.

Shared maternity care is usually given to women who are healthy and include no complications in pregnancy. Doctors or midwives involved in the care may charge some gap fees but the amount is likely to be less than obstetrician fees.

Obstetricians in public hospitals are the doctors having specialisations in pregnancies and birth. Such individuals are generally involved in providing care if a woman experience complications during the pregnancy. One needs to attend public hospital antenatal clinic and get referred by the local doctor for your initial consultation.

If you choose to select your own obstetrician, you need to have your baby at the hospital, with whom your obstetrician is affiliated. You can first choose your hospital and ask for a list of obstetricians.

Note: Without a referral from the local doctor, you won’t be able to take your first obstetric appointment. You also need to confirm the fees of private obstetricians and the Medicare item numbers. Once you have all this information, OSHC provider can confirm your gap fees.

Out-of-pocket Costs

Once the baby is born and doesn’t require to be formally admitted to hospital, any charges will not be incurred for the baby’s care. However, in case the baby needs treatment and requires to be admitted as an in-patient of the hospital, you may require to pay certain portion of the costs. This amount usually refers to the co-payment that is payable on your policy. The same is also applicable in case of twins or multiple births.

Services not covered in OSHC Pregnancy Care

- Out-of-hospital medical expenses including consultation and check-ups from obstetrician.

- Excesses and co-payments (if the baby is formally admitted to hospital)

- Fee for the paediatrician’s visit (on private health insurance policy)

Looking to add pregnancy cover in your OSHC? You can get the best quote at Getmypolicy.online.

At Getmypolicy.online, you can compare a wide range of OSHC plans by leading health insurance providers on different parameters and pick the one that meet your requirements.

For further assistance on upgrading your OSHC policy, you can get in touch with our experts today at support@getmypolicy.online.

That feeling is indeed exhilarating!

You’ve always dreamt of studying in Australia and the opportunity finally knocks at your door.

You got a Confirmation of Enrolment from the desired university to apply for student visa.

Every moment is now consumed preparing the application- collecting required academic certificates, evidence of sufficient funds & proving English language proficiency.

Did you make arrangement for the sufficient level of health insurance cover too?

But I am visiting Australia just to complete my studies. I’ve enough funds to take care of myself. Why would I need health insurance? You wonder.

Here’s why you need health cover!

The applicants of Australian student visa along with their dependents are required to have Overseas Student Health Cover (OSHC) for the entire duration of stay in Australia. If you fail to get a health insurance cover, you are at a risk of having your visa cancelled.

What is OSHC?

OSHC is a health coverage specifically designed to help international students cover the costs of medical and hospital care for the duration of stay in Australia.

With OSHC, an international student is covered for:

- Out-of-hospital medical services

- Ambulance services

- 100% of MBS fee for any in-patient services like surgery or extended care for an illness

- Public and private shared ward accommodation (only those private hospitals that are associated with OSHC insurance provider)

- Some Prosthetic devices

- Pharmaceutical benefits up to $50 to a maximum of $300/year for an individual and $600 for families or couples

Depending on the level of cover you choose, OSHC also include costs for general treatment like dental, optical and physiotherapy.

There are also other treatments covered but include a waiting period. These include psychiatric or pregnancy related. The waiting period begins from the first day listed on student visa.

Why it is necessary for international students to buy OSHC?

International students in Australia are not eligible for Medicare, Australia’s health care system that offers a range of medical services for free or at a lower cost.

And paying for emergency medical services can be really costly in Australia. This is when overseas student health cover comes to the rescue. It provides an access to medical treatment that is available and affordable in case any unfortunate situation happens.

How much does OSHC cost?

The cost of OSHC varies depending upon the type of cover you need. There are three different levels of health cover.

- Single – covers the main applicant i.e. overseas student

- Dual family – covers the overseas student and either one adult spouse/de facto partner or one or more children younger than 18 years’ old

- Multi-family – covers the overseas student and more than one dependant, including one adult spouse/de facto partner or one or more dependent children

Who are the top insurers of OSHC Australia?

Currently, there are six leading health insurance providers of OSHC:

How to make arrangements for OSHC?

You can choose to buy OSHC either from the education provider or OSHC approved provider. Regardless of your choice, it is mandatory to have a continuous coverage for the entire duration of stay in Australia. This particularly applies to those international students studying through two different institutions which make arrangements of insurance on student’s behalf.

If you are planning to choose your own OSHC approved provider, it can be quite tough and overwhelming to buy the best suitable one due to a wide array of insurance policies available. Hence, it is always advisable to compare health insurance plans to make sure you are covered for all medical contingencies.

At www.getmypolicy.online , you can compare wide range of OSHC plans by leading health providers and buy the one that perfectly fits your requirements. It serves you with unbiased comparison and also has quick and simplified buying process. And yes, there are no hidden costs too!

Reciprocal Health Care Agreements with Australia

If you belong to the country that has a reciprocal health care agreement with Australia, you are eligible to access some subsidised health services with Medicare. This includes emergency care or care for an illness that needs to be treated immediately. You may be still required to have OSHC as the cover is limited.

So now you have understood the importance of having a health insurance, make sure you don’t let it become a barrier to fulfil your international dreams by not purchasing the one.

If you need further assistance to buy the right OSHC plan, Give us a buzz today! We’ll come with the best solutions in no time.

Your planning to stay or work in Australia is going in a full-fledged manner. You have everything on the table except health insurance. You called your agent to discuss health covers. He comes, fully armed with forms and booklets, and start explaining policies to you from basic to the more complex ones.

And then…. the real struggle starts. You wrestle with tons of information and before you start understanding something, you are forced to weigh the additions or subtraction of each policy.

| More than 70% of overseas workers have trouble understanding what covered in their policy |

| 40% of visitors said they don’t understand changes in their coverage |

| While 50% of policy holders admitted their regrets for the decision on insurance benefits. |

You need to quickly submit evidence of health insurance cover to the immigration policy but, you are here wondering what suits you best or what you need to include in the cover. Right?

Well, there is no denial in that buying an overseas health insurance cover is complicated. Comparing the benefits of different plans, weighing monthly premiums against yearly deductibles make one go insane, especially when you’re short on time.

Must Read: Common Insurance Terms You Should Know: Overseas Health Cover

This is why; we have come up with few tips that can help you evaluate your options and choose the most suitable plan quickly. Take a look!

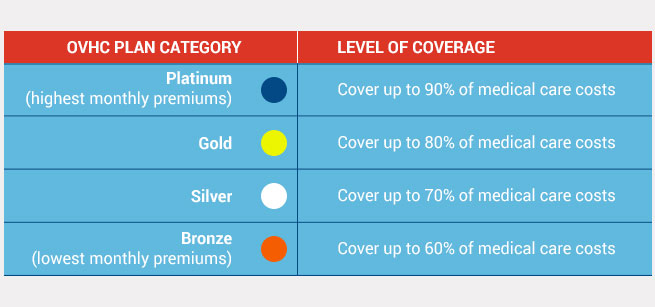

Choose the Right Category

Any health insurance plan typically consists of four categories: Bronze, Silver, Gold and Platinum and OVHC is no exception. These categories show how the policy holder (you) and the insurance company will share health care costs; however, they do not affect the quality of care.

Let’s understand each category precisely before making any decision.

- Bronze: Bronze plans are the basic ones with lowest monthly premiums but the highest costs when you get care. Such plans are recommended if you need few medical services and mostly the protection from bearing full costs at the time of sickness or injury.

- Silver: Silver plans include moderate monthly premiums and moderate costs to get care. The deductibles of this plan are usually lower than those of bronze plans. It covers about 70, 80 or 90 percent of total health care costs, depending on your income.

- Gold: Gold plans have the higher monthly premiums and lower costs when you get care. If you are willing to pay more each month to get your maximum costs covered at the time of medical treatment, gold plans provide great value. Besides, the amount of deductibles you pay before your plan pays are usually low.

- Platinum: Platinum plans come with the highest monthly premiums but the lowest costs when you get care. The deductibles in this plan are very low, means you start reaping its benefits earlier than any of the four categories mentioned above.

Understand Health Care Needs before Costs

You pay monthly premiums, even when you don’t use medical services that particular month. You pay out-of-pocket costs along with deductibles to access care. More often, we tend to overlook our health care needs and shift our entire focus on bills that are required to pay to the insurance company. However, the decision should be made on the basis of health care needs and not just the costs suitable to the pocket.

Compare Health Insurance Plans

It is extremely crucial to learn how each policy of different providers is different in regards to premiums and the services covered. When one has so many policies at hand, it is a common to go with the first few that come in the direction. However, when there is possibility of striking the best deal by comparing different plans, why not make use of it? Resources like GetMyPolicy.online allows you compare plans of leading providers like Allianz Care, Bupa, Nib, Medibank, and AIA to help you choose the one that best meet your budget and visa requirements.

Choosing the right health care coverage is one of the most important decisions you can make for you and your family to ensure a peaceful journey in Australia. You can save a lot of time by constricting the search to those plans that pay for your regular and necessary care. And then consider premiums and out-of-pocket expenses on the basis of budget and assets.

Australia is an exotic and beautiful nation! It’s a dream for many to live and work in this country!

There are many benefits for working and living in Australia! Who doesn’t like Lash greeneries, hills or lovely beaches to wake up! It’s a nation where individuals are also very friendly! So socializing in Kangaroos country becomes simple!

If you have been given an opportunity to migrate to Australia with your family members, you’d probably be working by the sweat of your brow to make the most out of this.

You desperately want the department of immigration to give your visa a green signal, so go through the criteria carefully to make sure you have all the documents you need to apply for the visa.

Wait… health insurance cover!!!

I am young and healthy. Why do I need that? You ask with uncertainty!

Well, more often applicants face delay in their visa processing as they fail to submit some crucial documents.

An adequate level of Overseas Visitor Health Cover (OVHC) is one of them.

All the temporary visas of Australia are subject to 8501 condition, which require an applicant along with the accompanying family members to have health insurance for the entire duration of stay in Australia. It assures a hassle-free access to Medicare (a publicly funded universal health care system in Australia) services during any of the following situations.

Health Deterioration Due to Unsuitable Weather

Weather is the most important factor that many immigrants overlook when moving to a different country. Australia’s climate is as diverse as its culture. The country has been labelled as one of the most vulnerable one to climate change due to high importance of its agriculture sector and prominence of its coast.

The changing climate can have significant repercussions on health like high blood pressure, headaches & migraines, asthma, eczema, and sometimes heart attacks and stroke too. This is where the benefits of having a health insurance can be clearly seen. It typically pays 80 to 90 percent of the costs after the deductible has been reached.

Injury due to accident

Accidents can happen to anyone. They are unanticipated and often result in severe injuries. This cause huge hospitalisation expenses be it private or public hospital along with corresponding medical bills. With an appropriate health insurance cover, you are not only backed against such bills but also get saved from financial hardships.

Dental emergencies

Imagine how irritating or upsetting it can be when something as small as a fragmented tooth can literally force you to book your return flight for treatment. All because you cannot afford the costs of the treatment in Australia. Having the dental emergency covered in your policy means you can continue to enjoy pain-free stay in Australia whilst getting quality treatment by the specialists.

Epilogue

With exponential increase in health care costs, it is essential to have a health insurance that can help you in the long run. So before you rush to buy one, why not compare multiple health insurance plans by leading providers like Bupa, IMAN, Australian Unity, Medibank and Allianz Global Assistance first to choose the one that best meet your budget and visa requirements.

Read More: 6 Most Important Terms to Consider for Australia Health Insurance Plan

At Getmypolicy.online, purchase the best health cover in less than 5 minutes by comparing a wide range of insurance policies on different parameters including:

- Doctor Services

- Accommodation

- Prescription Medicine

- Accident & Emergency Services

- Emergency Ambulance Services

- Out of hospital medicines

- In-patient psychiatric, rehabilitation and palliative care

You’d probably start wondering there must be some hidden catch, right?

But there’s not. It’s completely authentic and unbiased. Plus, the buying process is so simplified and there’s a guaranteed saving on investment.

Visit now and start exploring plans today!

Many international students studying in Australia enter a very exciting phase in their life when they graduate from their course and apply for a temporary graduate visa 485.

So,

What is a 485 Temporary Graduate Visa?

The 485 Temporary Graduate visa allows international students to live, study and work in Australia temporarily upon graduating from an Australian educational institution.

However, they will still need to arrange adequate overseas health insurance (OVHC Australia) for yourself and any family member, if applicable.

Students have around 2 months to plan for this visa as there is a necessity to lodge the 485 visa application before their student visa will expire. With such a short time, more often than not, students oversee the 485 visa health insurance.

The duration of your stay in Australia will be based on one of the three streams offered under this visa category, viz., Graduate Work, Post-Study Work, and Second Post-study Work.

But first, let’s see the eligibility criteria for a 485 visa:

- be younger than 50 years of age

- hold an eligible visa

- have held a student visa in the last 6 months

- have a recent qualification in a CRICOS-registered course

- nominate one stream only – it is not possible to change visa streams after you apply

- attach specified evidence when you apply

Types of 485 Visa Health Cover

| Temporary Graduate Visa (subclass 485) | Graduate Work Stream | Post-Study Work Stream | Second Post-Study Work Stream |

| Can work in Australia | Can work in Australia | Can work in Australia | |

| Can bring your family with you | Can bring your family with you | Can bring your family with you | |

| Have a qualification relevant to an occupation on the skilled occupation list | Need a recent degree a CRICOS-registered course | ||

| Stay | 24 Months | Between 2 to 4 years | Between 1 to 2 years |

| Processing Time | 17 to 19 Months | 9 to 14 Months | Undefined |

OVHC Australia:

All 485 visa applicants are required to purchase an Overseas Visitor Health Cover (OVHC) to meet their visa requirements. 485 visa applicants of both Graduate Workstream and Post- Study Workstream have to satisfy visa condition 8501 which mandates to buy the health insurance policy. The visa condition 8501 states that applicants should demonstrate that they have the adequate arrangement for health insurance for the entire period of their stay in Australia.

What is considered an adequate health arrangement by the Department of Home Affairs?

Your 485 visa health insurance policy must at least cover benefits equivalent to:

- public hospital treatment in an Australian State/Territory

- surgically implanted prostheses

- pharmacy – Pharmaceutical Benefits Scheme (PBS) listed drugs

- medical services, and

- ambulance services, including inter-hospital transfers.

Within the above specification, TR applicants can choose from a range of OVHC policies available in the market. But narrowing down to the right policy simply depends on the policy buyer’s health care needs.

485 Visa Health Insurance Requirements:

Health insurance requirements for 485 temporary graduate immigration visa effective March 21st, 2013 allows Post-Study Workstream applicants to live up to 4 years.

To meet 485.215 conditions, the visa application must be supported with evidence that the applicant:

- had adequate arrangements in Australia for health insurance and

- has had adequate arrangements in Australia for health insurance since the time the application was made.

That is, to cover the period between when the application was made and when the decision-maker is assessing the application (known as the time of decision).

The 485 visa health cover requirements for the secondary applicant are also the same – refer to 485.312

Types of OVHC Policies:

You can choose from the following overseas health insurance:-

A Low Range cover – Covers yourself and your families’ ambulance and hospital expenses. These policies also cost the lowest.

A Medium Range cover – Depending on the insurance provider, this level of policy will cover for Out of Hospital treatment (GP’s and specialist Doctor services) other than Hospital expenses and some prescription medicines. These policies cost in the median range between AUD 105 – $250 for a single cover policy.

A Top Range cover – More comprehensive coverage for private hospital treatment than the above two covers with more options of receiving benefits towards dental, optical and physio treatments (Extent of coverage vary according to the Insurance Provider). A top range cover is more expensive compared to the other two.

NIB OVHC, Medibank OVHC, Allianz Care OVHC, AIA, BUPA OVHC are leading Australian Health Insurance Providers that provide policies of all ranges from standard to comprehensive coverage.

OVHC Australia with an Auto-debit Option:

Unlike an OSHC policy, the visitors’ and workers’ health cover (OVHC) does not demand the policy buyer to pay the premium in full for the entire duration of stay. You can opt for an auto-debit option with your Health Insurance provider on a weekly, fortnightly, monthly, or yearly payment basis.

Lastly, always Compare & Buy:

It is always good to research and get the best insurance policy that suits your health care needs and budget. Choosing the right policy using a comparison resource like GetMyPolicy.online will help you save time, effort, and most importantly money.

Opting for the policy that aligns with your health needs now will help you save money at the time of purchase and the overhead costs if you require medical treatment at a later stage. You can get fast quotes, complete the purchase online and get a Visa letter within minutes. Make your OVHC Australia policy purchase hassle-free through GetMyPolicy.online.

If you are an overseas visitor, worker, or international student, you must have seen one of the conditions on your visa which mandates you to keep adequate overseas health insurance.

Moreso, are you curious about the health insurance waiting period for OSHC Australia and OVHC Australia? Wondering how long you have to wait before you’re covered by overseas health insurance?

Many of you must be unsure about what does a waiting period mean and why is it necessary to serve it before claiming for some specific services.

You’re not alone!

In this blog post, we’ll break down the waiting period for both types as well as pregnancy cover waiting period, so you know what to expect. Plus, we’ll give you a few tips on how to prepare for your coverage. Stay tuned!

Demystifying OSHC & OVHC Australia Waiting Period

What is a Waiting Period?

Overseas health insurance companies usually set out different types of conditions when awarding policies in order to make sure that only eligible people will benefit from them. They do this through various treatments or procedures which applicants should meet in advance before making claims on their policies. These terms are known as “waiting periods”.

Moreover, this also applies for OVHC Australia and OSHC Australia policies as well where you are obliged to serve the same number of days in between your arrival date and policy commencement date before becoming eligible under their respective terms & conditions.

When does a Health Insurance Waiting Period Apply?

It applies in two cases.

- If you start a new private insurance policy;

- If already covered and you wish to upgrade your policy to higher level cover.

When it is not applicable?

When you choose to change your policy provider to an equal or to a lower level of cover, you would not have to re-serve the waiting period that you have already completed.

Importance of Serving a Waiting Period

It’s important to understand that there is a waiting period for both OSHC and OVHC Australia. This waiting period is in place to ensure that people aren’t taking out insurance only when they need it, but are instead paying premiums all year round so as to avail policy benefits when they actually need it.

Additionally, the health insurance waiting period is in place for a reason – so make sure you’re fully aware of what’s included in your health cover before making any claims.

Types of Health Insurance Waiting Period

There are two types of waiting period viz.,

- Hospital waiting periods

- Extra cover waiting period

What is Hospital Waiting Period?

There is a hospital waiting period with both OSHC and OVHC. This is the time you have to wait after your arrival in Australia before you are able to make a claim for any medical expenses. The hospital waiting period usually starts on the day that you arrive in Australia, but it can vary depending on your international health insurance policy.

With OSHC, the hospital waiting period is typically two months, while with OVHC Australia it is typically six months. However, there may be some exceptions so it’s important to check your policy details carefully.

Generally, 12 months of waiting period applies in case of pregnancy care or if a person needs a hospital facility for some pre-existing conditions! It is recommended to check the specific policy details of the waiting period with GetMyPolicy.online.

Must Read: Pregnancy Care in OSHC! Essential Things You Need to Know!

What is the Extra Cover Waiting Period?

It differs with service providers and the level of cover! Although there are usually 6 months of waiting time for contact lenses, there will be at least 12 months of waiting time for hearing aids! For any psychiatric problem, some providers have 2 months of waiting period while some have none! You must log in to GetMyPolicy.online to compare between the best plans before buying!

What is a Pre-existing Condition?

Pre-existing condition is basically an illness or condition that you have had in the last 6 months before joining your current health insurance policy or before upgrading it.

For example: Sam had a back pain for which he was referred to a neurosurgeon by a GP. After getting the treatment done, Sam claimed against the hospital bills!

Since, the back pain existed 3 months before joining the current policy, Sam couldn’t claim for the hospital charges as it falls under Pre-existing condition.

What is Pre-existing Condition’s Waiting Period?

You or your doctor might not be aware of the condition, but it can be still considered as pre-existing! The reason because you hadn’t visited your doctor before joining the hospital policy or upgrading to higher hospital policy.

Generally, risk factors are not included as a pre-existing condition. For the new hospital policy holders, there will be no benefit for 12 months! In case, if you already have a hospital policy and then transferred to a higher level of cover, one may only receive the lower benefits of his/her previous cover for a pre-existing condition in the first 12 months on your new policy.

In case you have to admit in a hospital during the waiting period, then you should contact the insurer to check whether it falls under the benefit!

How To Avoid The Health Insurance Waiting Period?

For Pregnancy benefits, you must buy a new policy or upgrade your current policy prior to 12 months to avoid huge hospital costs! Some service providers also give child care benefits! For that, you need to check with the particular service provider!

Sometimes insurers run some offer and waive the waiting period to attract more customers! You can check those offer by logging in GetMyPolicy.online! Although it is merely impossible for the service providers to waive the whole 12 months waiting period, you still can hope to get the best possible deal!

It is always best to plan rather than spend! Isn’t it?

Wrap Up:

Whatever your choice is, we are here to help you. At GetMyPolicy, choose between the best government-registered OSHC & OVHC insurance providers. Also, compare plans, see available features, and know precisely what you pay for. That is not all. Upload your policy and get 15 FREE PTE Practice Tests!

Making a claim is an inevitable part of Overseas Health Insurance Cover. Do not hurry while claiming the services you avail. Follow this simple process and make a hassle-free claim!In this short post, we have listed the step-by-step guide to help you claim for your OSHC policy as well as OVHC Australia. Let us begin with OSHC for Australia.

There are 2 ways to claim for your Overseas Student Health Cover (OSHC) Policy:-

How To Claim Your OSHC for Australia Policy:

1. Online

- Access your online membership account via the policy provider’s website or mobile app

- Submit the claim form

- Receive a unique claim reference number on your receipts

- Scan and e-mail that receipt to the policy provider’s account

2. On-Campus

- Claiming in person, visiting On-Campus customer service location

You can make a claim of your OSHC for Australia policy by logging into the policy provider’s website and submitting the claim form! You will receive a unique claim reference number on your receipts. Scan and e-mail your receipt to the policy provider’s account! For OSHC policy holder’s there is an advantage of claiming in person after visiting the on-Campus customer service location!

If you have a policy with Allianz Care, visit their website and click ‘Make a claim’! (https://allianzassistancehealth.com.au/en/make-a-claim/)

In case you choose Ahm OSHC , you will find the details in ‘how to claim’. (https://www.ahmoshc.com.au/how-to-make-an-online-claim/)

How To Claim Your OVHC Australia Policy:

If you have an Overseas Visitor Health Cover (OVHC) Australia Policy, you have to claim through:-

1. E-mail

- Download the E-form from the website and print

- After filling up the details, scan the form and upload it

If you have a policy with Medibank, you can call them to make a claim! (https://www.medibank.com.au/life-income-funeral/make-a-claim/)

2. By Post

- download and print the claim form

- post it with receipts to the service provider’s address

Some service providers like BUPA has their App! * You can download and install it to make a claim! (https://www.bupa.com.au/health-insurance/cover/overseas-visitors/already-member)

If you have a policy with NIB, log in to My Account and make and claim! (https://my.nib.com.au/login?ReturnUrl=onlineservices)

At GetMyPolicy.Online, we always strive to provide you with the an easy comparison of OSHC & OVHC for Australia policies. Not only price comparison but aspiring international students, working & non-working visitor class can also compare policies on the basis of the features & benefits such as out-of-hospital, in-hospital medical services, accident & emergency department facility, waiting periods, refund policy, etc.

As an International student, many will be familiar with the Overseas Student Health Cover (OSHC). But we rarely think about the benefits covered by an OSHC policy except when we are faced with an illness or a medical condition which puts us in a situation of financial crunch. That’s when one gets introduced to the nitty-gritty of the insurance policy and terms such as claims and reimbursement starts to sound familiar.

One of the most frequent claim lodged as an Overseas insurance holder is for pharmacy bills. Yet understanding around the entitlements one receives as a policy purchaser towards the pharmacy bills is very vague. Or all pharmacy bills covered? If so, why do I always seem to get less claimable returns than the original bill? Or all pharmacy items covered? These are some of the questions that circle around the minds of International students while spending for their pharmacy bills out of pocket.

In this blog, we have broken down some crucial questions when it comes to coverage for pharmacy expenses and claiming for your pharmacy bills.

So, first off, what is covered?

Pharmacy bills containing prescription medicines prescribed by a doctor/GP while in Australia is covered under your OSHC policy. Which means, medicines that can be purchased over the counter without a prescription from a doctor cannot be reimbursed under this policy. For eg: Betadine, taken for a sore throat without a doctor’s advice.

What exactly is Prescription Medicine?

A prescription medicine refers to the medicines prescribed by the doctor requesting to be dispensed to the patient by the pharmacist. Such medicines need to be listed on the PBS (Pharmacy benefit Schedule) to get reimbursement for pharmacy expenses under the OSHC policy.

So, who pays first?

The student always pays off the pharmacy bill first and then, approaches the OSHC insurance provider for the claim benefits. The OSHC claims officer processes the pharmacy bills and reimburses the student a certain coverage amount.

What coverage can I get from OSHC providers against Prescription Medicine Costs?

Pharmacy expenses coverage always comes with a co-payment. It is a fixed amount paid by the student and the insurance company both, every time a medical service is claimed. Currently, for most of the OSHC providers, the minimum co-payment set by the Pharmaceutical Benefits Scheme (PBS) for international students is $40.30. Also, the maximum coverage one can get per pharmacy item listed in the bill is up to $50.

Still confused, let’s work it out with an example.

For instance, there are 3 items mentioned in a pharmacy bill- Drug A, Drug B and Drug C

Drug A costs $45

Drug B costs $32

Drug C costs $92 and the total bill amount is, $169

This is how co-payment works for this bill.

For Item 1 of the bill, Drug A, the student pays the first $40.30 and the OSHC provider pays $ 4.70

For Item 2, Drug B the student is supposed to pay the whole amount as it costs only $32, as it is less than the co-payment limit of $40.30. This means the student is not eligible for a claim for Drug B listed in the bill.

For Item 3, Drug C, the student pays the first $40.30 and the OSHC provider pays $ 50 as the maximum coverage limit per prescription item is set at $50. The rest of the excess amount will be paid by the student. Hence for Drug C, The student pays a total of $42 while the OSHC insurer pays $50.

It is important to remember that co-payment applies for every single prescription item listed in the pharmacy bill.

| Hence for this bill, the student receives an overall claim benefit of $ 54.7 back from the OSHC provider while $ 114.3, is his/her out of pocket expenses. |

Is there an annual limit to the claimable amount towards pharmacy benefits?

Yes, there is! Please see the table below for detailed info on member contribution, maximum coverage per pharmacy item and annual claim limit for single and family policy for each provider

| OSHC Provider | Member contribution | Maximum coverage per pharmacy item | Annual Claim limit (Single Policy) | Annual Claim limit (Family Policy) |

| Ahm | $40.30 | $50 | $300 | $600 |

| Allianz Global Assistance | $40.30 | $50 | $300 | $600 |

| Bupa | $40.30 | $50 | $300 | $600 |

| Nib | $40.30 | $50 | $300 | $600 |

| Medibank(Essential) | $30 | $70 | $300 | $600 |

How to know which drugs or medicines are covered by the Pharmaceutical Benefit (PBS) Scheme?

PBS has medicines listing on their website. You can visit here: http://www.pbs.gov.au/browse/medicine-listing to explore the same.

Easy Steps to Claim for Prescription Medicines

- Get your medicines prescribed by the doctor

- Purchase it from a pharmacist and obtain a receipt covering all the information you need to claim

- Complete a claim form available at your OSHC provider’s website along with the receipt.

- Get your co-payment amount

Seeking further assistance on any type of coverage for your OSHC policy? Get started with our experts today at support@getmypolicy.online.

Imagine, you are studying in Australia in a reputed university and then one fine day you need to call your parents saying that you cannot continue your stay in the country.

Something unfortunate happened. Your health took a debacle and you had to get treated in Australia, but your health insurance (OSHC policy) did not cover you for the expenses. Or you failed to renew and extend your OSHC and thereby got your visa cancelled by the immigration department for breaching 8501 visa condition.

What if you have to deal with the same situation while you study in Australia?

You’ll be devastated! Won’t you? As there was so much of hard work done to get the opportunity of studying overseas.

But the good news is, you can take precautions and avoid facing such consequences.

Most of the times, international students end up regretting with their OSHC plan as they either:

- Buy it in a hurry

- Buy just by relying on family or friends’ recommendation or

- Buy the one by focusing solely on low-cost

If you are one among the students, planning to purchase overseas student health cover to meet requirements of student visa, all you need to do is to look for the most suitable plan and spend wisely on it.

Must Read: Why Overseas Student Health Cover is Necessary to Get Australian Student Visa?

So, What Defines a Suitable OSHC plan?

A suitable OSHC plan is nothing but the one that covers all your needs and provide you with peace of mind knowing that you are financially protected for the entire duration of your stay in Australia at the time of medical emergencies.

And how will you ensure that the plan you selected is perfect for you?

Keep reading to find out!

Compare Policies of Different OSHC Providers

When it comes to choosing the best overseas health insurance plan, we often get intimidated by a wide range of options available. Sometimes we end up buying a plan which costs less but doesn’t offer comprehensive coverage or we pay substantial premiums only to realise later that we never required frills in our plan.

So, before zeroing in on one, it is imperative to compare Overseas student health insurance policies from leading providers to make sure of getting the adequate level of coverage during emergencies.

Execute a quote on www.getmypolicy.online to get feature by feature comparison across all OSHC provider. Here, you can get specific insights on coverage patterns when it comes to Public and Private hospital treatments, Out of Hospital coverage for pathology, GP services and specialist requirements such as MRI scans.

You can also learn about applicable waiting periods and refund clauses through the comparison tool on our site.

Compare their Services

A common factor that all OSHC providers have is they offer additional services or features in their plans. The difference however is they may not be equal in how they perform or what they may cover.

For instance, some insurance providers have a designated OSHC app that helps their members to:

- Submit and process claims easily and quickly

- Find the nearest doctors

- Access membership card with policy details anytime

- Get local emergency numbers, etc.

While some OSHC providers have home doctor services and on-campus support services added in their plans. To get an idea how you can compare such services, you can refer to the table given below:

| Service Features | Bupa | Medibank | AHM | Allianz Global Assistance | NIB |

| On Campus Support | No | Yes | No | Yes | Yes |

| Large network of qualified medical providers | Yes | Yes | Yes | Yes | Yes |

| Home Doctor service | Yes | No | No | Yes | No |

| 24/7 OSHC help line (interpreter services in a variety of languages) | Yes | Yes | Yes | Yes | Yes |

| OSHC app to submit claims | No | Yes | No | Yes | Yes |

| Dedicated OSHC website with resources | No | No | Yes | Yes | No |

| Emergency assistance (Doctors on demand) | No | No | No | Yes | No |

| Single parent cover | No | Yes | Yes | Yes | No |

| Online services to manage membership | Yes | Yes | Yes | Yes | Yes |

| Membership discounts towards other services | Yes | No | No | No | No |

Now that you know how comparison helps you to land on a policy that’s right for you, are you looking for a resource that can help you run such quote or service comparison quickly? Visit www.getmypolicy.online now & start comparing plans by leading health insurance providers to make a right decision.

For further assistance, you can also drop us an email at support@getmypolicy.online and get best solutions immediately.

The Victorian Skilled Migration Program for the fiscal year 2023-2024 is now accepting applications from both domestic residents in Victoria and international candidates.

Who Can Apply:

- Eligibility Criteria: Must be under 45, have competent English, and score at least 65 points on the Australian Government’s points test.

- Nomination from Victoria: Required for application.

- Application Process: Involves submitting an EOI to the Department of Home Affairs and an ROI for Victorian nomination.

- Required Documents: Passport, English language test, and Skills Assessment are mandatory. An employment contract and payslips are needed if you are currently working in Victoria.

- Time Limit: Must submit the visa application within 60 days of receiving the nomination.

Skilled Visa Processing Priorities in Australia: What’s New?

The Australian government has outlined specific priorities for processing skilled visa applications. Here’s a quick rundown:

- Healthcare & Teaching: Top priority is given to professionals in healthcare and teaching sectors, including roles like medical scientists, social workers, and school principals.

- Employer-Sponsored Visas: If you’re nominated by an accredited sponsor, your application will be fast-tracked.

- Regional Area Occupations: Jobs in designated regional areas are also given priority, making it easier for applicants willing to work in these regions.

- Permanent & Provisional Visas: Applications contributing to the migration program are prioritized, except for the Business Innovation and Investment (Provisional) visa.

- Other Applications: All other visa applications are processed thereafter.

For more information please visit official website:

Additional Information and Support

The program is expected to conclude in the early part of 2024, with the specific closure date to be announced in due course.

Detailed information about the program, encompassing eligibility criteria and key timelines, will be made available as soon as it is finalized.

For personalized consultation or further clarification, you are encouraged to reach out at +61-3-9602-3435 or initiate an online inquiry.

Source: Click Here